Key Insights

- A U.S. tokenization platform needs legal review, investor checks, custody planning, and transfer controls from the start. Treating compliance as a later task can lead to delays, rework, and investor distrust.

- The token should reflect the exact rights given in legal documents, including income, voting, resale, and redemption terms. If on-chain activity and legal records do not match, the platform can face serious operational and regulatory issues.

- Tokenization can make asset ownership easier to divide and transfer, but it does not promise an active market. Secondary trading needs eligibility checks, transfer rules, investor demand, and regulated trading support.

Tokenization is no longer a side topic for blockchain teams. In the U.S., asset owners, fund managers, real estate firms, and financial groups now see it as a practical way to represent ownership through digital tokens. A property, fund share, bond, commodity, or private asset can be divided into digital units, giving investors access to assets that once required higher capital, longer paperwork, and slower settlement.

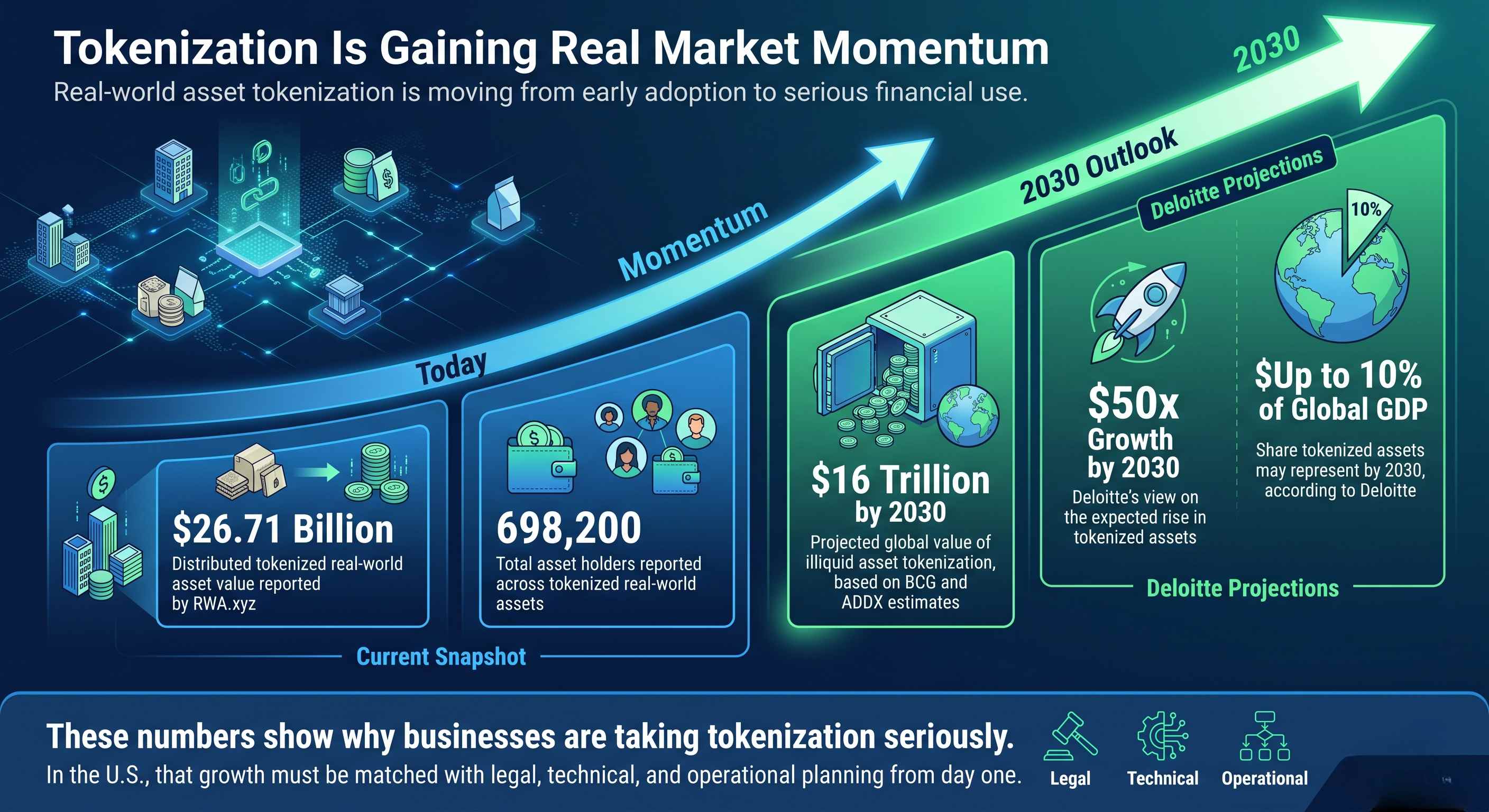

The market already shows real momentum. RWA.xyz reported about $26.71 billion in distributed tokenized real-world asset value and about 698,200 total asset holders. That tells us tokenized assets have moved well past the trial stage. BCG and ADDX have also estimated that illiquid asset tokenization may reach $16 trillion globally by 2030. Numbers like these explain why financial firms now treat tokenization as a serious business move, not just a blockchain experiment.

But a token is not just a digital record. In many U.S. use cases, it can represent income rights, ownership claims, voting power, or resale value. That brings the platform close to securities rules, investor checks, custody duties, and financial reporting. For this reason, compliance cannot sit at the end of the project. It must guide the platform from the first plan.

The U.S. Market Has More Regulatory Pressure

Launching a tokenization platform in the U.S. takes careful planning. Several regulatory areas can apply at the same time. A tokenized real estate share, for example, can touch securities law, investor eligibility checks, money transmission rules, custody standards, and trading restrictions. This makes the U.S. market more demanding than many other regions.

The long-term market outlook makes this even more important. Deloitte has noted that tokenized assets may grow fiftyfold by 2030 and may account for up to 10% of global GDP. That level of expected market growth means regulators, institutions, and investors are all paying closer attention. A platform cannot depend only on smart contracts or blockchain records. It needs legal structure, investor screening, transfer rules, document management, and audit-ready records.

A project that skips these steps can face delays, legal costs, blocked transactions, or loss of investor trust. A project that plans them early has a better chance to enter the market with confidence.

Legal, Technical, and Business Planning Must Work Together

A compliant tokenization platform needs legal, technical, and business planning to move together. The legal team defines what the token represents, what rights investors receive, and which limits apply to transfers. The technical team turns those rules into product functions such as wallet checks, investor permissions, token controls, dashboards, and transaction records.

The business team decides how the platform earns revenue, attracts issuers, supports investors, and manages assets after launch. Each part affects the others. A legal rule must appear inside the product. A business model must match the offering structure. A technical feature must support the compliance plan. This coordination reduces rework and gives the platform a cleaner path to market.

What a Tokenization Platform Does

It Turns Real Assets Into Digital Ownership Units

A tokenization platform helps represent real-world assets through blockchain-based tokens. These tokens can reflect ownership, income rights, voting rights, redemption rights, or transfer rights. Take real estate as an example. Instead of selling the entire property to one buyer, the asset owner can issue digital units linked to economic participation in that property.

The same model can apply to private funds, bonds, commodities, invoices, and revenue-backed assets. The asset remains off-chain, but the ownership record and transaction activity can move through the platform. This gives businesses a structured way to manage digital ownership without losing the legal connection to the actual asset.

It Gives Every User a Defined Role

A tokenization platform serves more than one user group. Asset issuers need a place to list offerings, upload documents, set terms, and manage investor activity. Investors need a simple portal to complete verification, review offering details, sign documents, make payments, and track holdings.

Compliance teams need tools to check identities, approve wallets, review transactions, and keep records. Administrators need access to ownership data, reports, payment history, distribution records, and transfer activity. Without these roles, the platform becomes only a token creation tool. That is not enough for a U.S. market launch.

It Manages the Token From Issue to Exit

A proper platform manages the full token lifecycle. It starts with asset onboarding and investor verification. Then it handles token issuance, payment tracking, ownership updates, income distribution, and transfer activity. Each step must connect with the next so the investment process remains organized.

Investor approval should connect with wallet permissioning. Token issuance should match payment confirmation. Ownership records should match legal documents. Transfer activity should follow the rules of the offering. This structure gives the token real business value. Without it, the token exists on-chain, but the investment process remains incomplete.

Choosing the Right Asset and Token Model

Start With the Asset, Not the Token

The asset decision should come before token design. Real estate, private funds, bonds, private equity, commodities, and revenue-backed assets all carry different rules. Each one has its own ownership records, valuation method, income pattern, legal documents, and investor duties. A tokenized apartment building, for example, will need property records, income details, title checks, and transfer rules. A tokenized fund will need offering documents, subscription terms, investor limits, and reporting rules. The platform must reflect these details from the start.

Match the Asset With the Right Token Type

The token model decides what the holder receives. A security token often represents investment rights, such as income, ownership, profit share, or voting power. A utility token usually gives access to a product or service. An asset-backed token links to a real or financial asset, such as property, gold, debt, or receivables. The name given to the token does not decide its legal treatment. The actual rights attached to the token matter more than the label.

Define Investor Rights Before Development Starts

The business should define holder rights before the technical team writes the first line of code. What does the investor own? Will they receive income? Can they vote on asset decisions? Can they sell the token after purchase? Is there a holding period? Can the issuer buy back the token later? These answers must appear in the legal documents, platform rules, and smart contract logic. If the rights stay vague, the platform can face confusion during issuance, reporting, and resale.

Keep Legal Records and Blockchain Activity Aligned

Legal ownership and on-chain activity must match. If only approved investors can hold the token, the platform must block transfers to unverified wallets. If income goes only to recorded holders, the ownership registry must stay accurate at all times. If resale is restricted for a fixed period, the token should not move during that period. This link between legal rights and platform behavior gives investors more confidence in the offering.

U.S. Legal and Regulatory Requirements

Token Classification Comes First

Before a tokenization platform enters the U.S. market, the token needs legal review. The main question is simple: what does the token give to the holder? If it carries ownership rights, income rights, profit participation, voting power, or resale value, securities rules can apply. This step should happen before fundraising, marketing, or platform launch. A wrong classification can lead to delays, legal costs, and forced changes later.

SEC Review Matters for Tokenized Assets

The SEC may review tokenized assets based on how they are sold, who buys them, what rights they carry, and what buyers expect from the issuer. Tokenized real estate, private funds, bonds, and revenue-backed assets often sit close to investment products. A token may live on blockchain, but its legal nature still comes from the rights and promises attached to it. This is why legal planning should guide product design from the start.

Pick the Right Offering Route

A U.S. tokenized offering usually needs a proper exemption or registration path. Regulation D is often used for private offerings to accredited investors. Regulation S is used for offshore offerings outside the U.S. Regulation A+ can support wider investor access, but it comes with more filing and disclosure work. A registered offering suits larger public market plans. The right route depends on the asset, investor group, budget, timeline, and resale strategy.

Check Investor Eligibility Early

Not every investor can buy every tokenized asset. Some offerings are limited to accredited investors. Some require jurisdiction checks, identity checks, or investment limits. The platform should check investor eligibility during onboarding, before payment and token issue. This keeps the process cleaner and reduces the risk of selling tokens to the wrong audience.

Control Transfers and Resales

Token movement after issuance needs careful control. Lock-up periods, resale limits, holding periods, and buyer checks can apply. A restricted token should not move freely to any wallet. The platform must apply transfer rules through wallet permissions, investor checks, and smart contract controls. Legal documents should support the same rules so the platform and paperwork stay aligned.

Review Other Regulatory Areas

Securities law is only one part of the U.S. compliance picture. A tokenization project can touch FinCEN rules, state money transmission laws, CFTC review, broker-dealer duties, ATS trading requirements, and custody standards. Not every rule applies to every project. The asset type, payment method, investor group, trading plan, and custody setup decide which areas need review.

Compliance Infrastructure for Investor Onboarding

Start With KYC and KYB Checks

Investor onboarding begins with identity review. KYC applies to individual investors. KYB applies to companies, funds, trusts, and other business entities. The platform must collect names, addresses, identity documents, company records, ownership details, and related proofs before investment access is granted.

This step protects the platform from unverified users and weak investor records. It also gives compliance teams a cleaner way to review who is entering the offering. For a U.S. tokenization platform, this is not just a formality. It is one of the first gates between a visitor and a financial transaction.

Screen Investors for Risk

A tokenization platform must check investor risk before allowing participation. This includes AML checks, sanctions screening, PEP review, and adverse media checks. These checks help spot users linked to financial crime, political exposure, restricted countries, or negative public records.

Risk screening should happen early in the onboarding flow. A risky investor should not reach the payment stage or receive a token allocation. Stopping a problem early saves time, protects the issuer, and gives the platform better control over compliance exposure.

Use Wallet Whitelisting for Approved Investors

After an investor passes verification, the platform can link that person or entity to an approved wallet. This process is known as wallet whitelisting. It means only verified wallets can receive or hold specific tokens.

This control matters for tokenized securities and restricted assets. If a token can move to any wallet, the platform may lose control over investor eligibility. Wallet permissioning helps block transfers to unknown users and supports rules for secondary activity. It keeps the token within the approved investor network.

Track Compliance After Onboarding

Compliance does not stop once an investor account is approved. Investor status can change. Wallet activity can look unusual. Sanctions lists can be updated. A platform must keep watching these changes after the first approval.

The system should support activity logs, transaction reviews, compliance alerts, and reporting tools. These records help teams understand what happened, when it happened, and who approved it. That kind of recordkeeping becomes useful during audits, investor disputes, and regulatory reviews.

Keep Digital Agreements and Investor Records Together

Every investor record should connect identity checks, eligibility status, wallet address, signed documents, payment activity, and token holdings. Subscription agreements, risk disclosures, investor acknowledgments, and tax forms should stay in digital form.

This gives the platform a complete investor file. If an investor asks for records, the team can find them quickly. If auditors review the offering, the platform can show the full history. A clean record also helps the issuer manage future distributions, transfers, and reporting.

Ready to launch a compliant tokenization platform in the U.S.?

Turn your real-world asset idea into a compliance-focused tokenization platform with investor onboarding, token issuance, wallet controls, payment flows, and admin dashboards. Blockchain App Factory helps businesses create RWA tokenization platforms that support legal, technical, and business needs from the first stage.

Technical Architecture of a Compliant Tokenization Platform

Asset Onboarding Module

The asset onboarding module is where issuers add asset details to the platform. This can include legal documents, valuation records, ownership proof, income terms, offering terms, and supporting files. It acts as the digital file for the asset.

Investors need this information before they commit money. Compliance teams need it to review the offering. Issuers need it to manage the asset after token issuance. If asset data is weak, the rest of the platform starts on shaky ground.

Investor Onboarding Portal

The investor onboarding portal guides users from sign-up to approval. It should collect profile details, run KYC or KYB checks, support document signing, connect wallets, and confirm investment eligibility.

The flow should feel simple for investors, but it must still capture enough information for compliance teams. Long forms can reduce investor interest. Missing checks can create legal risk. The platform needs the right balance between ease of use and complete verification.

Token Issuance Dashboard

The token issuance dashboard gives admins or issuers control over token offerings. It can include token quantity, token price, investor limits, sale dates, lock-up terms, accepted payment methods, and distribution rules.

This dashboard should connect with compliance checks. Tokens should only go to approved investors who meet the offering rules. The dashboard should also help teams monitor subscription progress, token allocation, and issuance status from one place.

Cap Table and Ownership Registry

A tokenization platform needs a reliable ownership registry. It should show who owns each token, how many tokens they hold, when they received them, and what restrictions apply.

For tokenized securities, this record supports investor servicing and legal administration. It helps with income payments, transfer reviews, tax reporting, and investor communication. The ownership registry must match blockchain activity and legal records.

Compliance Rules Engine

The compliance rules engine applies legal and business rules inside the platform. It can block transfers to unverified wallets, limit purchases to accredited investors, apply lock-up periods, and flag unusual activity.

This reduces manual checks for every transaction. It also helps the platform apply rules in the same way each time. For U.S. tokenization projects, this function is a major part of controlled token movement.

Payment and Settlement Module

The payment and settlement module handles investor subscriptions, payment confirmation, refunds, income payouts, and settlement records. It can support bank transfers, card payments, stablecoins, escrow accounts, or banking partners based on the platform model.

Every payment should match the investor record and token allocation. If an investor pays for 1,000 tokens, the system should show the payment, allocation, wallet, and ownership update in the same record trail.

Dashboards for Admins, Issuers, and Investors

Each user group needs a different dashboard. Admins need platform control, compliance reviews, user management, and reporting access. Issuers need asset records, offering status, investor lists, and distribution tools. Investors need portfolio views, signed documents, payment history, income records, and ownership details.

Good dashboard design reduces support requests and operating errors. It helps each user see only what matters to them. That makes the platform easier to manage and easier to trust.

Smart Contract Requirements

Permissioned Token Transfers

Smart contracts for U.S. tokenization platforms need more control than standard crypto tokens. A regulated token cannot move to every wallet on the internet. The platform must check who sends the token, who receives it, and whether both sides meet the rules of the offering.

Permissioned transfers help the platform manage this control. If the token represents real estate, fund interests, bonds, or other regulated assets, every transfer should follow investor eligibility rules. This protects the issuer and keeps token movement aligned with legal terms.

Whitelist-Based Investor Controls

A whitelist works like an approved holder list. Only verified investors and approved wallets can receive or hold the token. This gives the platform a practical way to stop transfers to unknown users, blocked regions, or investors who do not meet the offering rules.

This method also supports secondary transfers. Instead of reviewing each movement from scratch, the platform can check the receiving wallet against the approved list. If the wallet is not approved, the transfer does not go through.

Automated Distributions and Income Payments

Smart contracts can support income payments tied to token ownership. These payments can include dividends, rental income, fund returns, interest, or revenue share. The platform can use ownership records to calculate who should receive payment and how much they should receive.

This gives issuers a cleaner way to manage recurring payments. Investors can also see how their holdings connect to income activity. The payment process still needs accounting checks, but smart contract logic can reduce manual errors.

Lock-Up Periods and Transfer Restrictions

Many tokenized assets come with holding periods and resale limits. For example, some investors cannot sell for 12 months. Some tokens can move only to approved buyers. These rules should live inside the smart contract and the platform controls.

If a token is restricted, the contract should reject transfers that break the rules. This keeps the platform from relying only on manual review. It also reduces the chance of an investor selling to an ineligible buyer.

Freeze, Burn, Recovery, and Forced Transfer Functions

A compliant platform may need control functions for special cases. A freeze function can stop token movement during suspicious activity or legal review. A burn function can remove tokens after redemption, cancellation, or correction.

Recovery functions help address lost wallet access. Forced transfer functions may be needed for court orders, investor death, ownership correction, or compliance action. These features need strict access controls, since misuse can damage investor trust.

Smart Contract Audits and Upgrade Planning

Smart contracts should go through security review before launch. Code errors can lead to wrong transfers, payment mistakes, frozen assets, or security breaches. A third-party audit helps find issues before investor funds enter the system.

The platform should also plan for future changes. Regulations, token terms, and business needs can change after launch. Upgrade planning gives the platform a way to update rules without exposing investor assets to unnecessary risk.

Custody, Wallet, and Asset Security Requirements

Choosing the Right Custody Model

Custody decides who controls private keys and asset access. In self-custody, investors manage their own wallets. In third-party custody, a provider manages wallet access for users or institutions. Qualified custody may be needed for certain regulated or institutional asset structures.

The right model depends on the asset, investor profile, legal duties, and risk level. Retail investors may need simpler wallet access. Institutions may require formal custody, approval workflows, audit records, and account controls.

Institutional Wallet Infrastructure

Institutional investors often need more than a basic crypto wallet. They need user roles, approval chains, transaction limits, activity logs, and reporting tools. A fund manager, for example, may require two or more internal approvals before a token transfer.

A U.S. tokenization platform should account for these needs early. Wallet design affects investor trust, transaction safety, and daily operations. Weak wallet controls can create risk even if the token contract works correctly.

Multi-Signature and MPC Wallet Security

Multi-signature wallets require more than one approval before a transaction is completed. This reduces the risk of one person moving assets without review. MPC wallets split signing authority into separate parts, so no single device or user holds full control.

Both methods can reduce theft, internal misuse, and accidental loss. They are useful for high-value tokenized assets, issuer treasury wallets, custody accounts, and platform admin functions. The choice depends on security needs, user skill, and operating cost.

Private Key Recovery and Disaster Planning

Wallet access can fail for many reasons. A user can lose a device. An employee can leave. A private key can be misplaced. A cyberattack can interrupt access. The platform needs a recovery plan before any of this happens.

A good recovery process can include backup rules, multi-person approvals, emergency contacts, access logs, and written procedures. Investors need confidence that their holdings will not disappear after a simple access failure.

Asset Verification and Proof of Ownership

Security is not limited to wallets and keys. The asset behind the token must also be verified. For real estate, this can include title records, valuation reports, lease details, and insurance documents. For funds, it can include offering documents, ownership registers, and administrator records.

For commodities, proof may include storage records, inspection reports, and third-party audits. If the asset record is weak, the token loses credibility. Investors need proof that the token links to a real asset with valid ownership and documented value.

Payment, Settlement, and Distribution Flow

Support Fiat Payments for U.S. Investors

Many U.S. investors still prefer familiar payment methods. Bank transfers, ACH, wire payments, and card payments are common in private offerings and investment platforms. A tokenization platform should support these payment flows through banking partners or payment providers.

The payment record must connect with the right investor, offering, and token allocation. If an investor pays for 5,000 tokens, the platform should show the payment status, investor approval, token issue, and ownership record in one place. This reduces confusion for issuers, investors, and finance teams.

Plan Stablecoin Settlement With Care

Some platforms use stablecoins for faster settlement or crypto-native investors. Stablecoins can reduce settlement time and support digital asset users who prefer wallet-based payments. Yet they also bring compliance, custody, accounting, and reporting questions.

The platform must decide which stablecoins it accepts, which wallets can send funds, and how each payment is recorded. It should verify the investor before accepting payment. It should also match the wallet address, payment amount, token allocation, and investor file.

Manage Escrow, Subscriptions, and Refunds

Investor funds often need to stay in escrow until the offering reaches its conditions. This is common in private placements and asset-backed offerings. The platform should track subscription payments, failed payments, oversubscriptions, rejected investors, and refund requests.

This protects both sides. Issuers can confirm that funds are collected under the right terms. Investors can see whether their payment was accepted, pending, or returned. A clean escrow and refund process reduces support issues during fundraising.

Automate Income Payments to Token Holders

After the asset starts generating income, the platform should support payouts to eligible token holders. These payments can include rental income, dividends, coupon payments, revenue share, or redemption proceeds.

The system should calculate payments from ownership records and payment rules. For example, a holder with 2 percent of the tokenized asset should receive the matching share of distributable income after fees and agreed deductions. This makes payout handling easier for issuers and clearer for investors.

Match Blockchain, Banking, and Accounting Records

Every token movement should match the financial record behind it. The platform must compare blockchain transactions, bank entries, investor records, and accounting data. This helps catch mismatched payments, wrong allocations, and missing entries.

A tokenized asset platform runs on two record systems: on-chain and off-chain. Both must tell the same story. If the blockchain shows ownership but the payment record does not match, the platform has a problem to fix before reports are sent.

Secondary Trading and Liquidity Planning

Separate Primary Issuance From Secondary Trading

Primary issuance is the first sale of tokens from the issuer to investors. Secondary trading starts later, once investors want to sell or transfer their holdings. These two stages need different rules, systems, and partners.

Many businesses spend most of their time planning the first sale. Investors still care about what happens after purchase. Can they sell later? Who can buy from them? Are transfers restricted? A tokenized asset with no future transfer plan can lose appeal, even if the first offering looks attractive.

Use ATS Partnerships for Regulated Trading

In the U.S., tokenized securities often need a regulated trading environment. An Alternative Trading System, or ATS, can support trading for eligible digital securities under defined rules.

An ATS partnership can help the platform avoid informal wallet-to-wallet transfers. It can also support buyer checks, trading records, reporting, and transfer controls. This matters for platforms that want to support secondary market access without stepping outside the offering rules.

Check Eligibility Before Every Transfer

Secondary transfers still need investor checks. A token should not move from one wallet to another without reviewing the receiving party. The platform should check investor status, jurisdiction, holding period, wallet approval, and transfer limits.

This keeps trading activity tied to the original offering terms. If the token was sold only to accredited investors, the buyer in a resale should meet the same requirement, or any other rule set by the legal structure.

Set Honest Liquidity Expectations

Liquidity is often marketed too loosely in tokenization. Tokenization can make ownership easier to divide and transfer, but it does not create instant buyers. A market needs demand, asset quality, approved participants, trading support, and pricing confidence.

Investors should know this from the start. If secondary trading is planned, explain how it will work. If resale is limited, say so in plain terms. Honest communication protects trust and reduces disputes later.

Plan Liquidity Before Launch

Liquidity planning should begin during product design. The business should decide whether transfers will happen through an ATS, an internal bulletin board, manual approvals, or direct approved transfers.

It should also define who can participate, which restrictions apply, how pricing works, and how records are updated after each transfer. Without this planning, the platform may issue tokens successfully but struggle when investors ask for exit options.

Business Model and Platform Monetization

Earn Revenue From Token Issuance

Many tokenization platforms start earning during the asset onboarding and issuance stage. Issuers may pay fees based on token volume, fundraising size, legal complexity, or onboarding requirements. A platform handling multiple issuers can generate recurring revenue from new offerings entering the system.

This model works well for platforms focused on private markets, real estate offerings, or fund tokenization. The more active the issuance pipeline becomes, the more valuable the platform operations become over time.

Generate Ongoing Revenue Through Asset Management

Some platforms continue earning after issuance through recurring management fees. These fees can cover investor servicing, ownership administration, reporting support, distribution handling, and compliance activity.

Long-term tokenized assets often require ongoing support after the initial sale. Investors need reports. Issuers need administrative tools. Compliance teams need monitoring access. This creates a recurring revenue structure instead of a one-time issuance business.

Use Transaction-Based Revenue Streams

Platforms can also collect fees from subscriptions, settlements, transfers, and secondary trading activity. Even smaller transaction charges can become meaningful once the platform supports multiple offerings and active investor participation.

The fee model should stay simple. Investors and issuers should understand what they are paying for without reviewing complicated pricing tables. Clear pricing helps reduce disputes and improves platform trust.

Offer Custody and Administrative Services

Some platforms provide custody support, wallet management, reporting tools, or operational administration. These services can create another revenue stream, especially for institutional users who expect managed support instead of self-service access.

Administrative support may include investor communication, payment processing, tax reporting, document storage, and account management. Platforms serving funds, family offices, or asset managers often include these services as part of premium plans.

Choose Between White-Label and SaaS Models

Some businesses launch tokenization platforms for internal use only. Others license the platform to external issuers. In a white-label setup, clients use the platform under their own brand identity. In a SaaS structure, issuers access tokenization tools through a subscription model.

This allows the platform operator to support banks, investment firms, real estate groups, or private funds without directly managing the underlying assets. The decision depends on the target customer base and operating model.

Decide Between Single-Issuer and Multi-Issuer Platforms

A single-issuer platform supports one organization and its assets. This model is often easier during the early stages since operations remain more controlled. A multi-issuer platform supports multiple asset owners through the same infrastructure.

Multi-issuer platforms can generate larger revenue opportunities over time, but they also require stronger onboarding systems, compliance controls, and operational support. The platform structure should match the business goals from the beginning.

How Much Does It Cost to Create a Tokenized RWA Platform?

The cost to create a tokenized RWA platform can stay under control when the product is planned in phases. A business does not need every feature on day one. A lean version can start with asset onboarding, investor registration, token issuance, wallet support, and basic admin control. More complex features such as custody links, secondary trading, and automated payout systems can be added later.

For early-stage businesses, a practical MVP can start from $20,000 to $60,000, depending on the asset type, compliance flow, blockchain network, and number of user roles. The table below breaks down each feature with development time and cost ranges under $10,000.

| Features | Description | Duration | Cost |

|---|---|---|---|

| Platform Planning and Feature Scope | Defines asset type, user roles, token flow, admin needs, and launch plan. | 3 to 7 days | $800 to $2,000 |

| UI and UX Design | Covers basic wireframes, dashboard screens, investor flow, issuer flow, and admin layout. | 1 to 2 weeks | $1,500 to $4,000 |

| Asset Onboarding Module | Lets issuers add asset details, documents, valuation notes, ownership proof, and offering terms. | 1 to 3 weeks | $2,000 to $6,000 |

| Investor Registration Module | Allows investors to create accounts, add profile details, upload documents, and view approval status. | 1 to 2 weeks | $1,500 to $4,500 |

| KYC and KYB API Integration | Connects third-party verification tools for identity checks and business checks. | 1 to 3 weeks | $2,500 to $7,500 |

| AML and Sanctions Screening | Adds risk checks for sanctions, PEP status, and restricted user screening through API tools. | 1 to 2 weeks | $2,000 to $6,000 |

| Wallet Connection | Allows users to connect crypto wallets for receiving and holding tokens. | 1 to 2 weeks | $1,500 to $4,000 |

| Wallet Whitelisting | Adds approved wallet controls so only verified wallets can receive restricted tokens. | 1 to 2 weeks | $2,000 to $6,000 |

| Token Creation Module | Lets admins create tokens, set supply, price, asset link, and offering details. | 2 to 3 weeks | $3,000 to $8,000 |

| Basic Smart Contract Development | Covers token minting, transfer rules, token burning, and basic ownership logic. | 2 to 4 weeks | $4,000 to $9,500 |

| Smart Contract Review | Checks contract logic, access control, transfer rules, and common security issues. | 1 to 2 weeks | $2,000 to $8,000 |

| Investor Dashboard | Shows token holdings, payment status, documents, profile details, and basic portfolio view. | 1 to 3 weeks | $2,500 to $7,000 |

| Issuer Dashboard | Lets asset owners view offerings, investor lists, documents, and subscription status. | 1 to 3 weeks | $2,500 to $7,000 |

| Admin Dashboard | Gives platform owners access to users, assets, approvals, token issue, and settings. | 2 to 4 weeks | $4,000 to $9,500 |

| Document Management | Stores offering documents, investor files, subscription forms, and signed records. | 1 to 2 weeks | $1,500 to $5,000 |

| E-Signature Integration | Connects digital signing tools for agreements, disclosures, and subscription documents. | 1 to 2 weeks | $1,500 to $5,000 |

| Payment Gateway Integration | Supports card, bank, or basic fiat payment tracking through a payment provider. | 1 to 3 weeks | $2,500 to $8,000 |

| Stablecoin Payment Support | Allows approved wallet payments using supported stablecoins and records payment activity. | 1 to 3 weeks | $2,500 to $8,000 |

| Subscription Management | Tracks investor commitments, payment status, accepted subscriptions, and rejected entries. | 1 to 3 weeks | $2,000 to $7,000 |

| Basic Distribution Module | Helps admins record income payments, dividend entries, or payout history for token holders. | 1 to 3 weeks | $2,500 to $8,000 |

| Cap Table and Ownership Registry | Tracks token holders, token quantity, ownership percentage, issue date, and transfer status. | 2 to 4 weeks | $4,000 to $9,500 |

| Basic Compliance Rules | Applies investor approval status, wallet checks, holding limits, and transfer restrictions. | 2 to 4 weeks | $4,000 to $9,500 |

| Notification System | Sends email alerts for approvals, payments, document updates, and token activity. | 1 to 2 weeks | $1,000 to $3,500 |

| Audit Logs | Records user actions, admin changes, approval history, transfers, and payment updates. | 1 to 2 weeks | $1,500 to $5,000 |

| Cloud Hosting Setup | Sets up server, database, storage, deployment, backup, and basic monitoring. | 1 to 2 weeks | $2,000 to $7,000 |

| Security Testing | Reviews platform access, APIs, user data, wallet flow, and common security risks. | 1 to 2 weeks | $2,000 to $8,000 |

| Post-Launch Support | Covers bug fixes, minor updates, monitoring, API fixes, and small improvements after launch. | Monthly | $1,000 to $7,500 per month |

Step-by-Step Launch Roadmap

Define the Asset Class and Business Structure

The first step is deciding what type of asset will enter the platform. Real estate, private equity, commodities, bonds, and revenue-backed assets all follow different legal and operational structures.

The business should also define how the platform will operate. Will it support one issuer or many issuers? Will it focus on institutional investors, accredited investors, or broader participation? These decisions affect legal planning, onboarding flow, custody setup, and platform design.

Complete Legal Review Before Development

Legal review should happen before technical development begins. The token must be classified correctly under U.S. regulations. The business should review securities treatment, investor eligibility rules, transfer restrictions, offering structure, and possible licensing obligations.

This step prevents expensive rework later. Building the platform before understanding the legal structure often leads to delays and operational problems.

Define Investor Rights and Offering Terms

The platform should clearly define what token holders receive. This can include ownership participation, income rights, voting rights, redemption access, or transfer permissions.

These rights should appear in legal documents, smart contract logic, and investor records together. If the platform says one thing and the legal agreement says another, investor trust can weaken quickly.

Prepare the Technical Structure

After legal planning is complete, the technical structure can move forward. This includes investor onboarding systems, token issuance modules, compliance controls, ownership registries, payment tools, reporting systems, and admin dashboards.

Each module should support the legal and business model selected earlier. The technical side should not operate separately from compliance and investor management requirements.

Build Compliance and Onboarding Workflows

Investor onboarding should include identity verification, AML checks, wallet approval, document signing, and investor eligibility review. The platform should also support ongoing compliance monitoring after onboarding is complete.

A good onboarding process balances security and usability. Investors should move through the process without confusion, but the platform must still collect complete records for compliance teams.

Develop and Review Smart Contracts

Smart contracts should reflect the operational rules of the offering. This includes transfer restrictions, payment handling, lock-up periods, ownership tracking, and investor permissions.

Before launch, independent audits should review the contract code for logic errors, security risks, and operational weaknesses. Small contract issues can create major financial problems once investor funds enter the system.

Connect Custody, Payments, and Reporting Systems

The platform should connect with custody providers, banking partners, payment systems, and reporting tools. These integrations help manage subscriptions, settlements, income payouts, ownership updates, and investor communication from one operating environment.

Disconnected systems create reporting problems and manual work. Connected systems improve operational accuracy and reduce reconciliation issues.

Test the Platform With a Pilot Issuance

Many businesses begin with a smaller pilot offering before a full public launch. This helps test onboarding flows, payment handling, investor communication, token transfers, reporting activity, and compliance controls under real operating conditions.

Pilot launches help teams identify weak areas early. Fixing operational problems before scale reduces future disruptions.

Monitor Operations After Launch

The work does not stop after launch. The platform should continue reviewing investor activity, compliance records, smart contract performance, payment flow, and transfer behavior.

Regulations, investor expectations, and market conditions can change over time. A platform that continues improving its operations stays in a better position for long-term growth.

Conclusion

A compliant tokenization platform in the U.S. needs more than blockchain development. It needs the right asset model, legal review, investor checks, smart contract controls, custody planning, payment systems, and post-launch monitoring working together from the start. Each part supports the next. Legal terms guide the platform rules. Investor onboarding protects the offering. Smart contracts control token activity. Payment and ownership records keep the business organized. For companies planning to enter the U.S. tokenization market, this level of planning can reduce risk and build investor confidence. Blockchain App Factory provides Real World Asset Tokenization Services for businesses that want to create compliant, asset-backed tokenization platforms with the right mix of legal-aligned workflows, technical infrastructure, and market-ready platform features.

Vimal J is the Head of Sales at Blockchain App Factory, with 10+ years of experience in sales, client strategy, and Web3 business growth. He helps startups, enterprises, and project founders choose the right blockchain solutions for their goals, bringing a practical market perspective to topics like token development, crypto launches, and Web3 adoption.