Key Insights

- RWA tokenization moved crypto beyond speculation by bringing bonds, real estate, credit, commodities, and funds on-chain. It gave blockchain a stronger role in asset ownership, settlement, and capital access.

- Banks, asset managers, fintech firms, and fund issuers are using tokenization to reduce manual work and reach wider investor groups. Their involvement has made RWAs one of the most serious areas in digital finance.

- Tokenization divides high-value assets into smaller digital units and supports faster trading across regions. This gives qualified investors easier access to markets that were once slow, expensive, or restricted.

In 2026, real-world asset tokenization moved from a niche crypto topic to a major finance story. For years, crypto was tied to coin trading, price swings, and short-term hype. Real-world assets gave the market a different base. They brought bonds, property, private credit, commodities, and fund shares onto blockchain networks.

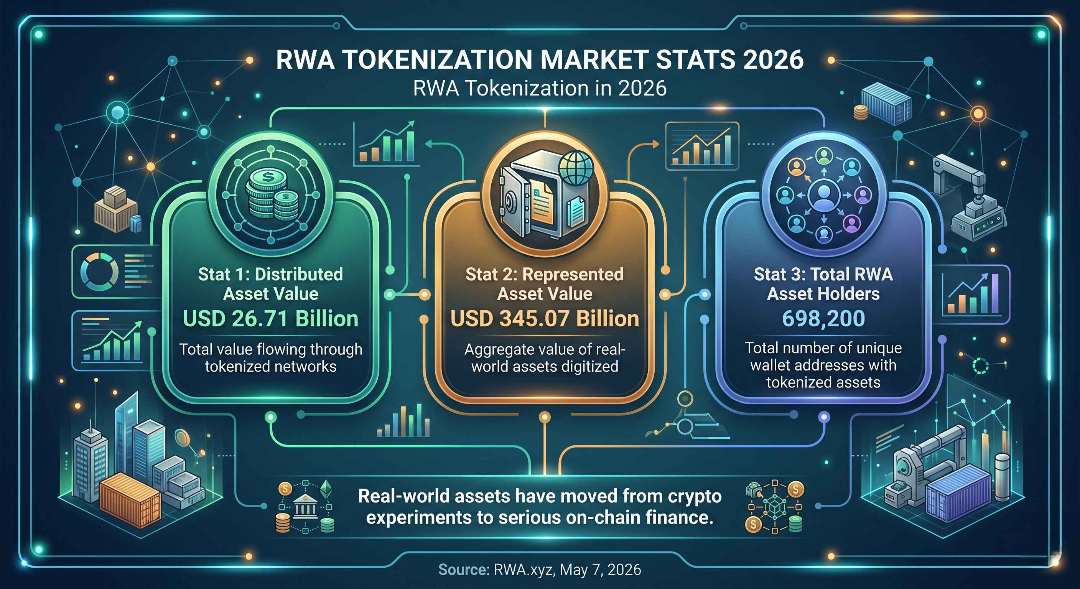

By May 7, 2026, RWA.xyz tracked USD 26.71 billion in distributed asset value, USD 345.07 billion in represented asset value, and 698,200 total asset holders across tokenized real-world assets. These numbers show that RWAs are no longer a small experiment. They have entered serious investor territory.

This change gave crypto a more practical role. Investors were no longer looking only at tokens with no link to the real economy. They started paying attention to assets with income, ownership rights, and legal claims behind them.

From Speculation to Utility: The Institutional Shift

Institutions changed the tone of the market. Banks, asset managers, fintech firms, and fund issuers began treating blockchain as financial infrastructure. The focus moved away from pure trading. It moved toward ownership records, faster settlement, and easier asset transfers.

That shift mattered. It gave tokenized assets more trust and more serious attention. Large firms wanted systems that could handle real money, real assets, and regulated financial activity.

How USD 185 Billion Entered the Blockchain Economy

The USD 185 billion figure came from steady adoption across several asset classes. Tokenized treasury products gained traction first. Private credit, real estate interests, commodities, and fund units followed.

Issuers wanted a faster way to reach investors. Investors wanted assets tied to real value. Tokenization gave both sides a practical meeting point. It turned slow, paper-heavy assets into digital units that can move across blockchain networks with fewer delays.

The Rise of Regulated Digital Ownership

As more capital entered the RWA market, legal structure became more important. Investors wanted proof of backing, valid ownership rights, custody records, and compliance checks.

This created a new form of digital ownership. A token was no longer just a symbol in a wallet. It became a record tied to an asset, a contract, or a financial claim. That shift made RWAs easier for institutions to discuss, test, and adopt.

Why Investors Are Moving Beyond Traditional Markets

Traditional markets still play a major role, but many investors dislike their limits. Settlement can be slow. Access can be restricted. Fees can stack up. Private markets often stay closed to smaller investors.

Tokenized markets offer a different model. Assets can be split into smaller units. Ownership can be recorded digitally. Trading can take place through blockchain-based platforms. For many investors, RWAs feel like a practical bridge between conventional finance and digital markets.

Understanding RWA Tokenization in Simple Terms

What Real-World Asset Tokenization Actually Means

Real-world asset tokenization means representing an asset through digital tokens on a blockchain. The asset can be a building, bond, fund share, invoice, gold reserve, or loan portfolio.

Think of it like a digital ownership receipt. The asset stays in the real world. The token records the right, claim, or share linked to that asset. This makes ownership easier to divide, transfer, and track.

How Physical and Financial Assets Become Digital Tokens

The process starts with the asset itself. The issuer checks ownership, value, legal status, and investor rights. After that, tokens are issued to represent a share or claim.

A building can be divided into digital units. A treasury product can be represented through tokens backed by government securities. Gold can be linked to tokens backed by metal held in custody. The token acts as a digital wrapper around the asset.

The Technology Behind Tokenized Ownership

Smart contracts manage many parts of tokenized ownership. They record transfers, investor rules, payment flows, and trading limits. Blockchain networks store the ownership history.

Legal agreements and custodians connect the token to the asset. The blockchain keeps the record. The legal structure gives that record value in the real world.

Why Blockchain Became the Ideal Settlement Layer

Blockchain works well for tokenized assets since it records transactions across a shared network. Traditional settlement often needs brokers, banks, clearing systems, and transfer agents. That can add time and cost.

On-chain settlement reduces many of those steps. Ownership records can update faster. Investors can move assets with fewer delays. Issuers can manage transactions with less manual work.

Difference Between Traditional Asset Markets and Tokenized Markets

Traditional markets depend on several middlemen. They often involve long settlement periods, paperwork, and restricted access. Tokenized markets use digital tokens to record ownership and move assets across blockchain networks.

The main difference is control over access, speed, and recordkeeping. Traditional markets often feel like mailing documents across offices. Tokenized markets feel closer to sending a verified digital file. Both can work, but one fits modern finance better.

The Explosive Growth of the RWA Market in 2026

How the Market Reached USD 185 Billion

The RWA market reached USD 185 billion in 2026 through steady demand from both institutions and investors. This growth did not come from hype alone. It came from assets people already knew: treasury bills, private credit, real estate, money market products, and fund shares.

Institutions wanted safer blockchain use cases. Investors wanted assets tied to real value. Issuers wanted faster access to capital. These needs met in one place, and tokenized assets became the answer.

Main Industries Behind Tokenization Adoption

Finance led the RWA market in 2026. Treasury products, bonds, private credit, and money market funds attracted the most attention. These assets already had trust in traditional markets, so they moved on-chain faster than many others.

Real estate came next. Property has high value, but it often needs large capital and long holding periods. Tokenized ownership made it easier to divide property interests into smaller units.

Commodities gained attention too. Gold, precious metals, and reserve-linked assets gave investors a familiar store of value in digital form. Invoices, luxury assets, and carbon credits joined the market, but financial assets stayed ahead.

Institutional Capital Entering RWAs

Institutional capital changed how people viewed RWAs. Large firms did not enter the market for short-term trading alone. They saw tokenization as a better way to issue, manage, and move assets.

Asset managers used tokenized funds to reach digital investors. Banks tested blockchain for settlement and collateral. Fintech firms created new investment channels. This activity gave RWAs a more serious image than earlier crypto trends.

Why Global Investors Prefer On-Chain Assets

Global investors like on-chain assets for three main reasons: easier access, faster movement, and smaller ownership units. Many traditional investments stay locked behind high minimums, regional limits, or slow processes.

Tokenized assets reduce some of those barriers. A qualified investor in one market can gain access to assets from another region through digital platforms. Ownership feels less restricted and more suited to modern finance.

The Shift From DeFi Hype to Asset-Backed Stability

DeFi once gained attention through high yields and bold claims. Many of those returns depended on token demand, market mood, or reward programs. That model became harder to trust after several market shocks.

RWAs brought a calmer story. Many products are linked to bonds, loans, real estate, or other income-producing assets. Investors can understand where the return comes from. That made 2026 a turning point for crypto finance.

The Most Popular Real-World Assets Going On-Chain

Tokenized Real Estate and Fractional Property Ownership

Real estate has always attracted investors, but the entry cost can be too high. Buying into a property project often needs large capital, legal work, and long timelines.

Tokenized real estate divides ownership into smaller digital units. An investor can hold a fraction of a property instead of buying the full asset. This makes property investing less closed off and more practical for a wider group of investors.

Treasury Bills and Government Bonds on Blockchain

Treasury bills and government bonds became some of the most trusted RWA products. They are familiar, income-based, and backed by governments. That gives them an advantage in a market where trust matters.

On-chain treasury products give investors access to bond-like exposure through digital tokens. For crypto users, this feels more stable than chasing unknown tokens with unclear value.

Tokenized Gold, Commodities, and Precious Metals

Gold and precious metals have long been used as stores of value. Tokenized versions bring these assets into digital markets without removing their real-world backing.

A tokenized gold product can represent a claim on physical gold held by a custodian. The investor holds the digital token, and the metal stays in secure storage. This removes many problems linked to storage, shipping, and physical handling.

Private Credit Markets Entering DeFi

Private credit became one of the fastest-growing RWA areas. It covers loans made outside public bond markets, often to businesses seeking capital.

By moving private credit on-chain, platforms can connect lenders and borrowers through digital markets. Investors gain access to income-producing loan products. Borrowers get another route to funding beyond banks and private lending networks.

Stocks, Equities, and ETFs Becoming Tradable 24/7

Stocks, equities, and ETFs are moving into tokenized formats. Traditional markets run on fixed hours, holidays, brokers, and settlement windows. Many digital investors now expect access at any time.

Tokenized equities can trade outside normal market hours, based on platform rules and local regulations. This does not remove market risk, but it changes the access model. For investors used to instant apps and digital wallets, that difference matters.

Luxury Assets and Fine Art Fractionalization

Fine art, rare watches, classic cars, wine collections, and other luxury assets were once limited to wealthy buyers. Tokenization divides these high-value assets into smaller ownership shares.

An investor may not own a full painting or rare collectible. They can still hold a piece of its value through a digital token. This gives luxury assets a wider investor base and creates new ways to trade rare items.

Carbon Credits and Sustainable Asset Tokenization

Carbon credits are entering blockchain markets as companies look for better tracking and easier trading. These credits represent emissions reductions or offsets.

Tokenization can make ownership records easier to follow. It can reduce confusion around duplicate claims and unclear records. For companies focused on climate goals, tokenized carbon credits bring digital finance into sustainability markets.

Why Institutions Are Investing Heavily in RWA Tokenization

Faster Settlement and Lower Operational Costs

Institutions care about time, cost, and risk. Traditional settlement can pass through brokers, banks, transfer agents, custodians, and clearing systems. Each step adds work. Each delay adds cost.

Tokenized assets reduce many manual tasks. Ownership changes can be recorded on blockchain networks with fewer back-office checks. This matters most at large volume. A small cost saving on one trade can become a major saving across thousands of trades.

Access to Global Liquidity Without Borders

Tokenized assets can reach investors across regions, subject to local rules. This gives issuers a wider buyer base than many private markets allow.

For investors, the appeal is access. A fund, bond, loan product, or property interest from another market can become easier to buy through a digital platform. Cross-border access still needs legal review, but the process can feel less closed than older channels.

Better Audit Records and Market Visibility

Blockchain gives institutions a shared record of asset activity. Transfers, ownership updates, and payment flows can be checked over time. That helps auditors, fund managers, and compliance teams follow the movement of assets.

This kind of record does not remove every reporting duty. It gives firms a cleaner trail to review. In markets where records sit across several systems, that alone can make a real difference.

Higher Yield Opportunities for Investors

Many RWA products offer income tied to real assets. Treasury products can pay bond-linked returns. Private credit can produce loan income. Real estate can create rent-linked payments.

This gives investors a return story they can understand. The yield does not depend only on token demand or market excitement. It comes from assets that already exist in traditional finance.

Less Dependence on Traditional Banking Infrastructure

Tokenized markets give institutions another way to issue, move, and settle financial products. Banks still play a role, especially in custody, compliance, and fiat access. Yet blockchain rails reduce some reliance on older systems.

This matters for firms operating across several countries. Cross-border transactions often face banking hours, currency steps, and settlement delays. Tokenized systems can reduce some of that friction.

Why Major Financial Firms Are Entering the Space

Major financial firms are entering RWA tokenization for three reasons. Clients are asking for digital access. Issuers want faster distribution. Asset managers want better ways to manage ownership records.

Many firms are testing tokenized funds, bonds, collateral systems, and settlement models. They are not treating RWAs as a side trend anymore. They see them as a practical part of future market infrastructure.

Ready to bring real-world assets on-chain?

Turn real estate, bonds, credit, commodities, or funds into blockchain-based digital assets with Blockchain App Factory’s RWA Tokenization Services. Build a compliant, investor-ready platform for the tokenized economy.

How RWA Tokenization Works Step by Step

Asset Identification and Legal Structuring

The process starts with choosing the asset. It can be a property, bond, loan portfolio, commodity, fund share, invoice, or artwork. The issuer then reviews ownership, asset value, legal status, and investor rights.

This stage matters most. A token has little value without a valid claim behind it. Legal documents define what the token holder owns, receives, or can claim.

Creating Digital Ownership Rights

After the legal review, the issuer creates digital ownership rights. These rights explain the token holder’s position. The token may represent income rights, repayment rights, a fractional interest, or a claim on an asset.

This step turns the token into more than a digital label. It links the token to real value through contracts, custody records, and investor terms.

Smart Contract Setup and Compliance Rules

Smart contracts manage token activity. They can record transfers, apply investor limits, manage payment rules, and restrict trading to approved users.

Compliance rules are often added at this stage. These can include identity checks, regional limits, investor category checks, and transfer restrictions. Serious RWA projects need these controls from the start.

Custody, Verification, and Asset Backing

The underlying asset must be verified and held properly. Real estate may need title records and legal agreements. Gold may need vault records. Bonds may need regulated custody.

Investors need proof that the token is backed by the asset it claims to represent. Without that proof, trust breaks quickly.

Secondary Trading on Blockchain Platforms

After issuance, RWA tokens can trade on approved blockchain platforms or marketplaces. This gives investors a possible exit route after the first sale.

Private assets are often hard to sell in traditional markets. Tokenized units can make resale easier, but trading still depends on regulation, buyer demand, and platform rules.

Yield Distribution and Automated Settlements

Many RWA tokens are linked to income. This can include rent, interest, loan repayments, dividends, or bond payments.

Digital systems can distribute these payments based on token ownership records. Smart contracts can manage payment timing and holder lists. Investors get a more direct payment process, and issuers reduce manual administration.

The Technologies Behind RWA Tokenization

Smart Contracts and Automated Financial Logic

Smart contracts handle many tasks inside RWA platforms. They follow written rules and act once those rules are met. In tokenized markets, they can record ownership transfers, apply investor checks, manage yield payments, and control trading limits.

This reduces the need for repeated manual work. A transfer that once needed several approvals can move through a programmed process. The result is a cleaner system for issuers, investors, and platform operators.

Stablecoins as the Payment Layer for RWA Markets

Stablecoins play a major role in tokenized asset markets. They give investors a digital form of money that usually tracks fiat currencies, most often the US dollar.

Many RWA platforms use stablecoins for buying assets, paying yield, and settling trades. This helps investors avoid constant exposure to volatile crypto prices. It gives the market a cash-like layer that works across blockchain networks.

Token Standards and Cross-Platform Use

Token standards define how digital assets behave. They set rules for transfers, ownership records, wallet support, and platform use.

Without common standards, every tokenized asset would work in a different way. That would make trading, custody, and reporting harder. Shared standards give platforms a common format, so tokenized assets can move with fewer technical issues.

Permissioned and Public Blockchain Networks

RWA projects use both public and permissioned blockchain networks. Public chains allow wider market access. Permissioned chains limit activity to approved users.

Financial institutions often prefer permissioned systems for compliance and privacy. Public networks attract projects that want wider reach and deeper market activity. Many RWA issuers now compare both options before choosing where to issue assets.

AI and Data Analysis in Asset Tokenization

AI and data analysis help RWA platforms review risk, asset quality, pricing changes, and investor activity. These tools can scan large amounts of data faster than manual teams.

For example, a private credit platform can use data models to review borrower health. A real estate platform can track occupancy, rent payments, and market prices. This gives issuers and investors better information before decisions are made.

Oracle Networks and Live Asset Pricing

Blockchain networks need outside data to price real-world assets. Oracle networks bring that data on-chain. They can feed asset prices, interest rates, commodity values, exchange rates, and market indexes into smart contracts.

A tokenized gold product needs current gold prices. A tokenized credit product needs payment and rate data. Oracles connect blockchain records with real market information, so RWA products stay aligned with the assets behind them.

The Biggest Benefits of Tokenized Assets

Fractional Ownership for Retail Investors

Fractional ownership is one of the main reasons investors care about tokenized assets. Many high-value assets need large capital in traditional markets. Real estate, private credit, fine art, and funds often sit out of reach for smaller investors.

Tokenization divides these assets into smaller digital units. A retail investor can buy a smaller share instead of the full asset. This gives more people a path into markets that were once limited to wealthy investors and institutions.

24/7 Global Market Access

Traditional markets run on fixed hours. They close on weekends and holidays. Tokenized markets can run around the clock, based on platform rules and local regulations.

This matters for global investors. A person in Asia, Europe, or the Middle East does not always want to wait for a market in New York or London to open. Digital asset markets match the pace of online finance.

Better Liquidity for Hard-to-Sell Assets

Some assets are hard to sell quickly. Real estate, private loans, art, and infrastructure stakes often need long sale processes. Finding a buyer can take weeks or months.

Tokenization can divide these assets into smaller units. Smaller units are easier to list and trade. Liquidity is never guaranteed, but tokenized ownership can make private markets less rigid.

Lower Entry Barriers for Wealth Creation

Many traditional investment products come with high minimums, long forms, and limited access. Tokenized assets reduce some of those barriers.

Investors can access smaller positions. Issuers can reach a wider pool of qualified buyers. This makes asset ownership feel less closed off, especially for younger investors who already manage money through digital apps.

Faster Cross-Border Transactions

Cross-border finance often moves slowly. Banking hours, payment networks, currency conversion, and settlement rules can delay transactions.

Tokenized systems can move value across regions faster. Investors can settle trades through digital wallets and blockchain networks. This cuts down waiting time and reduces the number of parties involved in the process.

Trackable Asset Ownership Records

Blockchain records create a trackable history of ownership and transfers. Investors can see how tokens moved. Platforms can review records for reporting and audits.

This gives RWA markets a more organized recordkeeping model. Instead of checking several disconnected systems, participants can refer to one shared ledger. That helps with trust, compliance, and investor reporting.

Lower Middleman Fees and Admin Costs

Traditional markets often involve brokers, custodians, transfer agents, administrators, and clearing systems. Each one adds cost.

Tokenized systems can reduce some of those layers. Smart contracts can handle parts of transfers, payment distribution, and ownership updates. For large institutions, even small savings per transaction can add up fast.

The Leading Sectors Benefiting From RWA Tokenization

Banking and Financial Services

Banks and financial firms are among the first major users of RWA tokenization. They are testing blockchain-based systems for bonds, funds, collateral, payments, and settlement.

The reason is simple. Financial products already depend on records, ownership rights, and transfers. Tokenization gives firms a digital way to manage these parts with less manual work. Banks are not trying to replace the whole financial system overnight. They are looking for faster ways to issue assets, track ownership, and settle transactions.

Commercial Real Estate

Commercial real estate is a natural fit for tokenization. Office buildings, hotels, warehouses, and housing projects often need large amounts of capital. They can also be hard to sell quickly.

Tokenization divides property interests into smaller digital units. This can bring in more investors and reduce the pressure on one buyer or one lender. A large property deal becomes easier to share across a wider investor base. For property owners, this can create new funding options. For investors, it can make real estate access less expensive and less rigid.

Global Trade and Supply Chain Finance

Trade finance still relies on heavy paperwork, slow approvals, and delayed payments. Invoices, shipping records, purchase orders, and receivables often pass through several parties.

Tokenization can turn these trade assets into digital records that are easier to verify and finance. A business waiting on invoice payment can raise funds against that invoice through a tokenized model. Investors gain access to trade-linked products. Businesses get another route to working capital. This matters most for small and mid-sized firms that often wait too long for payment.

Insurance and Risk Management

Insurance firms are studying tokenization for claims, reinsurance, risk-sharing, and policy-linked products. These areas depend on records, triggers, payouts, and trust between parties.

Blockchain-based records can help verify claims and track risk exposure. Smart contracts can handle certain payout rules once agreed conditions are met. The insurance market still needs careful legal work. But tokenization gives insurers a new way to manage data, payments, and asset-linked risk.

Renewable Energy and Infrastructure Funding

Renewable energy projects need large capital before they produce income. Solar farms, wind projects, grid upgrades, and battery storage often take years to finance and build.

Tokenization can divide these projects into smaller investment units. This gives more investors a way to support infrastructure funding. It can also help project owners reach capital outside traditional lenders. Energy-linked tokens can be tied to revenue, credits, or project ownership rights. That makes renewable energy funding more accessible for qualified investors.

Emerging Markets and Global Capital Access

Many businesses in emerging markets struggle to reach global investors. Local funding can be limited. Bank loans can be expensive. International capital can be hard to access.

Tokenization gives issuers a digital route to present assets to global investors. This can include real estate, credit products, infrastructure projects, trade assets, or commodities. For emerging markets, the value lies in wider access. A local project no longer has to depend only on local capital. It can reach qualified investors through regulated digital platforms.

How DeFi and RWAs Are Merging Into One Financial System

The Move From Pure Crypto to Asset-Backed DeFi

DeFi started with crypto-native assets. Lending pools, swaps, staking programs, and yield farms mostly dealt with tokens created inside blockchain markets.

RWAs changed the picture. Bonds, credit products, real estate interests, and treasury assets entered the same systems. DeFi gained a link to assets that already exist outside crypto. This made DeFi more practical. It no longer had to depend only on token demand and trading activity. It gained access to income from real financial products.

Yield Farming With Real-World Financial Products

Yield farming once relied heavily on token rewards. Those rewards often rose fast during market excitement and dropped just as quickly.

RWA-based yield works differently. Returns can come from treasury bills, private loans, rent, trade finance, or other asset-backed income streams. This gives investors a more grounded income source. The risk still exists. But the source of return is easier to understand than many earlier DeFi yield models.

Institutional Lending Using Tokenized Collateral

Tokenized assets are entering lending markets as collateral. A tokenized bond, fund share, credit product, or treasury asset can support borrowing on blockchain-based platforms.

This creates a more asset-backed credit model. Lenders can review the collateral behind the loan. Borrowers can use digital assets without selling them. For institutions, this is a practical bridge. It connects traditional collateral with blockchain-based lending.

Stable Returns Replacing Volatile Crypto Strategies

Crypto returns can swing sharply. Many strategies depend on token prices, trading volume, or short-term market interest.

RWA-linked returns often come from loans, bonds, rent, or other income-producing assets. That makes them more attractive to investors who want steadier income. This does not remove risk. Credit risk, market risk, legal risk, and platform risk still matter. But RWAs give DeFi a more stable base than pure reward-driven models.

The Rise of Hybrid Finance Models

Hybrid finance combines regulated assets with blockchain-based ownership and settlement. It does not reject traditional finance. It adds digital rails to parts of the process.

Banks, asset managers, fintech firms, and DeFi platforms can all take part. A fund can hold regulated assets, issue digital tokens, and settle activity on-chain. This model is likely to grow as more firms test RWAs. The market is moving toward a mix of legal structure, asset backing, and blockchain records.

How Businesses Can Prepare for the Tokenized Economy

Build Blockchain-Ready Financial Infrastructure

Businesses need the right internal systems before they enter tokenized markets. Digital assets do not work well with outdated spreadsheets, slow payment tools, and disconnected records.

A company should review its accounting systems, custody process, payment rails, wallet setup, and investor portals. These tools must support digital ownership records and blockchain-based transactions. This work does not need to happen all at once. But early preparation helps a business avoid confusion once investors, partners, or regulators start asking serious questions.

Understand Compliance Before Tokenization

Compliance must come before token issuance. A real-world asset token can carry legal duties linked to securities rules, investor checks, tax reporting, custody, and ownership rights.

Businesses should know who can buy the token, where it can trade, and what documents investors need. They should also define how income, voting rights, repayments, or claims will work. Skipping this step creates risk. A token tied to a real asset is not just a marketing tool. It is a financial product with legal weight.

Choose the Right Blockchain Network

Not every blockchain fits every RWA project. A company tokenizing real estate has different needs from a company issuing tokenized credit or fund shares.

The choice should be based on cost, security, user activity, compliance support, settlement speed, and institutional acceptance. Some businesses will prefer public networks for wider access. Others will choose permissioned systems for more control. The asset type should guide the decision. The investor base and legal setup matter just as much.

Create Investor Trust Through Verified Records

Investor trust comes from proof. Businesses need verified asset details, legal documents, custody records, audit reports, and regular updates.

Investors want direct answers. What backs the token? Who holds the asset? What rights does the token holder receive? How are payments handled? What happens if the issuer fails? A business that answers these questions early will stand out. In tokenized finance, trust is built through records, not slogans.

Use RWAs for Capital Formation and Growth

RWA tokenization can give businesses another way to raise capital. A company can tokenize revenue streams, property holdings, invoices, credit assets, or infrastructure projects.

This can reduce dependence on banks, private lenders, or closed investor networks. It can also help businesses reach qualified investors across more markets. For growing companies, tokenization offers a practical funding route. The value lies in real assets, proper structure, and investor confidence.

Conclusion

RWA tokenization has moved crypto closer to real finance by bringing bonds, real estate, credit, commodities, funds, and other valuable assets onto blockchain networks. The rise of USD 185 billion in on-chain assets shows that investors and institutions now want more than speculation. They want asset-backed ownership, faster settlement, wider access, and better records. For businesses, this shift opens a practical path to raise capital, reach qualified investors, and create digital asset models with real market value. Blockchain App Factory provides RWA Tokenization Services for companies that want to issue, manage, and launch tokenized real-world assets with the right technical setup, legal structure, and investor-ready platform.

Vimal J is the Head of Sales at Blockchain App Factory, with 10+ years of experience in sales, client strategy, and Web3 business growth. He helps startups, enterprises, and project founders choose the right blockchain solutions for their goals, bringing a practical market perspective to topics like token development, crypto launches, and Web3 adoption.