Key Insights

- The market now spans financial assets, physical assets, rights based products, and even resource access. This makes RWA a broad market structure, not a single niche.

- Legal wrappers, custody, compliance, data, and redemptions matter more than the token alone. A strong product links the digital claim to a real asset in a clear and usable way.

- They improve access, settlement, ownership records, and usability across finance and commerce. The weak ones only add a token without fixing the underlying market problem.

Real world assets have become a major theme in digital asset markets. Many people still treat RWA as another term for tokenized U.S. Treasuries. That view is too narrow. The market now covers debt, commodities, real estate, payment tools, collectibles, intellectual property, research rights, and, in some cases, compute and storage.

The recent growth helps explain the attention. RWA.xyz reported $26.71 billion in distributed asset value, $345.07 billion in represented asset value, and 698,200 asset holders on March 31, 2026. Tokenized U.S. Treasuries alone reached $10.00 billion on January 28, 2026. These figures show real traction. They also show that the market is still early.

The main shift is straightforward. Tokenization is no longer just about putting an asset on a blockchain. The bigger issue is how that asset gets issued, tracked, transferred, used, and redeemed. That turns RWA from a narrow product story into a broader market structure.

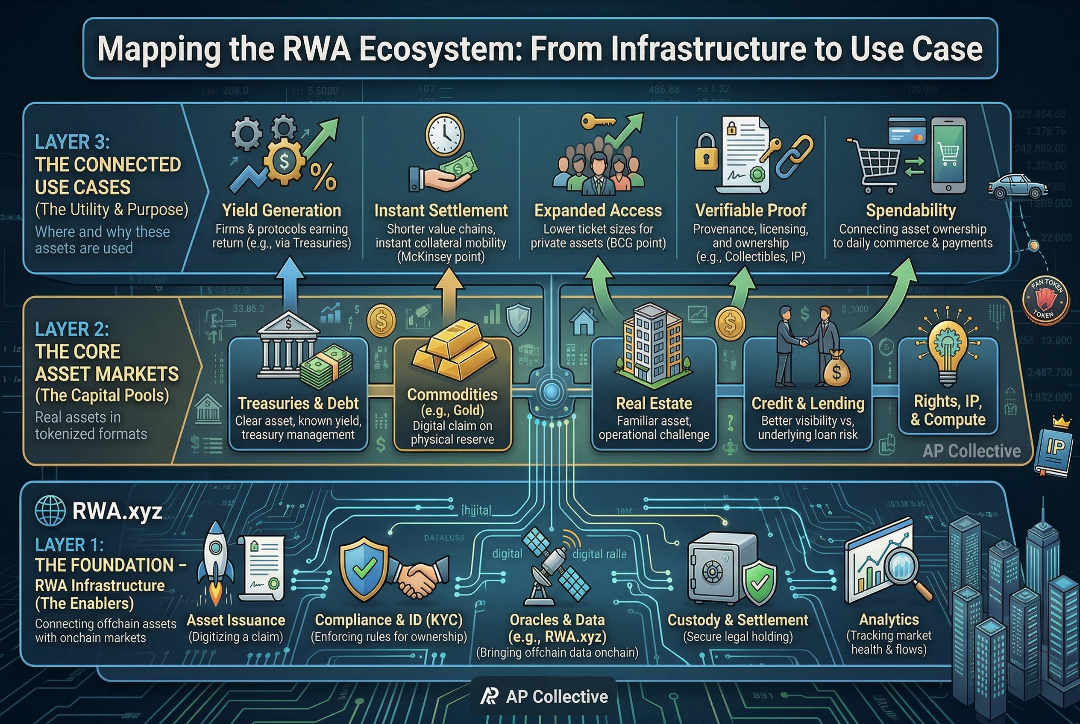

This article explains the RWA ecosystem through three layers. Infrastructure forms the base. Markets bring assets onchain. Use cases show how those assets become useful products for firms and investors.

What Is the RWA Ecosystem?

The RWA ecosystem is the full set of systems, issuers, assets, and applications that connect offchain value with onchain markets. That value can take different forms. It can be a financial claim, such as a Treasury fund or credit product. It can be a physical asset, such as gold or real estate. It can be an intangible right, such as IP, royalties, or research claims.

This broader definition matters. Many discussions reduce RWA to a small set of fund products. That misses how tokenization works in practice. A tokenized asset is rarely just a token. It usually sits inside a larger structure that includes legal wrappers, custody, transfer rules, identity checks, pricing, and redemption terms.

A simple way to read the market is through three layers:

- Infrastructure: issuance, compliance, oracles, custody, settlement, and analytics

- Markets: Treasuries, commodities, credit, real estate, rights based assets, and resource markets

- Use cases: yield, payments, collateral, fractional access, provenance, licensing, and commerce

This structure helps readers separate strong products from weak ones. A strong RWA product has a clear offchain claim, a defined legal structure, and a real use in the market. A weak one has a token, but no clear rights or redemption path.

Why Infrastructure Sits at the Base of the Stack

Infrastructure is the least visible part of the RWA market, but it matters most. It includes the systems that make tokenized assets usable for issuers, investors, and businesses. That means issuance rails, investor checks, transfer controls, reserve reporting, market data, custody, and analytics.

A tokenized Treasury product shows why this matters. The token is only one piece. The product still needs a legal structure, a custodian, pricing data, transfer rules, identity checks, and reporting. Infrastructure connects all of those parts.

This layer matters for three main reasons:

- It defines what the token holder actually owns

- It connects onchain records with offchain assets or rights

- It supports reporting, redemptions, and market access

Data tools matter here too. Platforms such as RWA.xyz and DeFiLlama help users track market size, product categories, and flows. These services do not issue assets, but they make the market easier to measure and compare.

Infrastructure sits at the base of the stack for a simple reason. It decides whether tokenization works in a real market or stays a concept.

The Main Asset Markets in RWA

The financial core of RWA rests on four areas: Treasuries, commodities, credit, and real estate. These markets attract capital since the underlying assets are already familiar. Tokenization changes the wrapper, not the basic asset.

Treasureis lead in scale and clarity. Commodities offer a simple reserve backed model. Credit opens larger opportunities but carries heavier risk. Real estate draws strong interest but stays hard to structure and trade.

Tokenized Treasuries

Tokenized Treasuries are the clearest RWA success so far. They give investors blockchain based access to U.S. government debt. This category reached $10.00 billion by January 28, 2026.

Their appeal is simple. The asset is familiar, the yield is clear, and the product fits digital treasury management. Firms can hold cash in a more flexible format and use these products in collateral or treasury workflows.

The limits are clear too. Most products require identity checks, follow issuer rules, and have restricted transfers. The token improves access and speed, but the product still depends on traditional custody, fund structures, and legal controls.

Commodities

Commodities, especially gold, fit tokenization well. A gold backed token gives users a digital claim on a physical reserve. That makes the product easy to understand and easier to move across digital platforms.

The main value lies in access and portability. Users can buy smaller amounts, store value in wallets, and move claims more easily than many traditional ownership records allow.

This category highlights a core RWA rule. The token is only as strong as the reserve behind it. Storage, audits, holder rights, and redemption terms matter more than the token format alone.

Credit

Credit shows both the promise and the limits of RWA. A tokenized credit product often represents repayment claims, interest streams, or exposure to lending pools. That gives private credit a more digital format for reporting and distribution.

The appeal is strong. Investors get better visibility, easier transfer, and wider access to private market exposure. Yet the hardest parts of lending remain unchanged. Borrowers still need underwriting. Payments still need servicing. Defaults still need legal enforcement.

This makes credit one of the best tests in the market. Better rails can improve access and reporting, but they cannot fix weak assets or poor underwriting.

Real Estate

Real estate has long been a popular tokenization idea. The appeal is clear. Property is valuable, familiar, and hard to access in small sizes. Tokenization can lower entry size and make ownership records easier to manage.

The problem is complexity. Real estate is local, regulated, and operationally heavy. In most cases, the token represents an interest in a legal entity that holds the property, not the deed itself.

Real estate products usually fall into four types:

- fractional ownership in property holding entities

- income or price exposure

- transaction rails for buying and selling

- digital records for title or settlement support

Tokenization can improve access and reporting. It cannot make property liquid or simple by itself.

Payments and Spending Rails

Payments make tokenized assets more useful in the real economy. This part of the market connects digital balances with spending, settlement, and treasury activity.

The value is practical. Firms can move working capital more easily. Users can spend through wallet linked tools. Platforms can settle cross border flows faster.

This category matters since it turns asset ownership into daily use. A tokenized Treasury product can generate yield. A payment rail gives users a reason to keep capital inside digital systems after that yield is earned.

Physical Collectibles

Collectibles show how blockchain records can support real markets outside finance. A token tied to a rare card, watch, or signed item can track provenance, custody, and ownership history.

The value here is proof, not cash yield. Buyers want to know the item is authentic and tied to a valid claim.

The weak point is obvious. The token moves faster than the object. Storage, insurance, inspection, and redemption still happen offchain. A strong collectible product needs trusted custody and clear terms.

Fan Tokenization

Fan tokens bring RWA closer to sports, media, and community products. These assets often represent access, rewards, membership, or participation.

The best products offer clear benefits:

- event access

- loyalty rewards

- membership features

- digital items tied to teams or creators

This category works only when the token carries real utility. Without that, it becomes a speculative badge.

IP, Science, and Creative Rights

Rights based assets are one of the most ambitious parts of RWA. This category includes IP, royalties, research rights, and licensing claims.

The appeal is strong. Tokenization can create cleaner records for ownership, funding, and revenue sharing. It can also open new models for creators and research groups.

Still, the structure must be clear. Readers should ask four questions:

- what right does the token represent

- who controls the underlying asset

- how are payments handled

- what legal protection exists in a dispute

This category has strong upside, but only when legal rights match the digital claim.

Compute and Storage

Compute and storage sit at the edge of the RWA market. These products tie tokens to real machine resources such as GPU power or storage capacity.

This is a frontier category, not the center of the market. It fits a broad RWA view since it turns scarce offchain resources into digital market access.

The use cases are straightforward:

- renting idle GPU capacity

- paying for distributed storage

- matching resource supply with demand

- creating access rights to real services

The main risk is service quality. Buyers care about uptime, speed, and reliability. A token cannot cover weak performance.

Ready to see where real estate investing is heading?

Tokenized property platforms are gaining serious attention in 2026 as investors and founders look for new ways to access, manage, and trade real estate exposure. Read the full article to understand why this segment is attracting so much startup activity.

The Use Cases That Connect the Entire Ecosystem

The RWA market makes more sense once readers stop viewing each category on its own. The deeper story sits in shared use cases. Different assets move through different legal structures and serve different buyers, but many of them solve the same market problems. They improve access, speed up settlement, tighten ownership records, and create new ways to fund or use value through software based systems.

Yield

Tokenized Treasuries lead this segment today. They give firms and investors a way to hold short duration government debt through digital rails. That matters for treasury desks, funds, and crypto native firms that want a yield bearing asset in a programmable format. The growth in tokenized Treasuries shows how strong this use case has become. By January 28, 2026, the category had reached $10.00 billion in total value. That figure explains why so much of the current RWA market starts here.

Settlement

Many legacy asset transfers still move through slow, layered systems. Tokenization can shorten that chain. McKinsey has pointed to round the clock transfer and instant collateral mobility as two of the clearest gains in tokenized markets. That matters in fund operations, payments, and secured finance. Time has value in capital markets. Faster movement can reduce idle cash, tighten reporting, and make collateral more useful across platforms.

Access

Tokenized formats can lower ticket sizes and widen distribution. This matters most in private market assets such as real estate and credit. It matters in collectibles and rights based markets too. BCG has stressed this point in its work on tokenized funds. A smaller investor can gain entry into products that used to sit behind higher minimums and slower subscription models. Access does not mean openness in every case. Many products still use strict investor screens. It does mean the market can reach buyers through new channels.

Spendability

A digital asset becomes more useful once it can support payment flows, treasury movement, or real commerce. This is where payment rails matter. Stablecoins and tokenized cash products play a major role here, and tokenized yield products can feed into the same system. A business can hold value in digital form, earn on that value, and then move it into settlement or spending tools with less friction than older systems often allow. That is a real shift in how working capital can move.

Verifiable

This one runs through collectibles, fan assets, IP, research rights, and some property products. In these categories, the token often acts as a record of who owns what right, what item, or what share of future value. That record can support transfers, licensing, funding, and resale. The use case is less about cash yield and more about proof. In many markets, proof is the product.

These shared use cases show why the stack matters. The market is not just issuing tokens. It is rebuilding how assets are packaged, distributed, and used.

What Still Holds the Market Back

The first barrier is legal clarity. A token can record a claim, but a legal system still defines whether that claim stands up in practice. This issue runs through every RWA category. A Treasury token needs a valid fund structure. A credit token needs enforceable loan rights. A property token needs a sound ownership wrapper. A collectible token needs a real link to the object in custody. The blockchain records transfers well. Courts, contracts, and regulated entities still protect the offchain asset.

Liquidity is the second barrier. Market value and market depth are not the same thing. A category can show strong headline growth and still offer thin exit options at the product level. This issue matters most in private credit, real estate, and niche rights based markets. Tokenization can improve transfer mechanics. It does not create steady buyer demand on its own. A healthy market still needs active venues, clear price discovery, and enough capital on both sides of the trade.

Fragmentation is the third barrier. Issuers use different chains, different transfer rules, different custody models, and different data standards. This makes comparison harder for buyers and slows adoption for institutions. Infrastructure providers are trying to fix part of that problem through better reporting, common data views, and stronger interoperability. The market still feels split across platforms and rule sets. That friction is real, and it raises costs for users who want to move across products.

User experience is the fourth barrier. Many tokenized products still ask users to pass through wallet setup, identity checks, issuer rules, network fees, and redemption terms that vary from one platform to another. Experts can tolerate that complexity. Mainstream users and most firms will not. Product design matters here as much as legal design. A system that works well on paper can still fail in the market once onboarding feels slow or unclear.

The fifth barrier is asset fit. Some assets adapt to tokenization more cleanly than others. U.S. Treasuries have shown strong early fit. Gold also fits a reserve backed model well. Private credit, real estate, and IP rights carry more legal and operational weight. Compute markets still need stronger proof of reliable service quality. This uneven pace is normal in an early market. It tells readers where the stack has real traction and where it still faces harder tests.

A simple set of questions can help readers judge any RWA product:

- What legal claim does the token represent?

- Who controls the offchain asset or right?

- How do transfers and redemptions work?

- What creates real liquidity for the product?

- What happens if the issuer, servicer, or custodian fails?

These questions cut through marketing and force the structure into view.

Where the Market Is Heading

The next phase of RWA growth will likely stay concentrated in categories with clean structures, clear demand, and strong links to existing financial activity. Tokenized Treasuries fit that description today. They combine familiar underlying assets, known yield, and a direct use in treasury management and collateral systems. That is why they have become the lead product in the market and the standard reference point for new entrants.

The second area to watch is payments. The market will grow faster once tokenized value can move through business and consumer workflows with less friction. Stablecoins already play a major role in that shift. Tokenized cash and wallet based payment tools will likely pull more RWA activity into daily use. That change matters for firms as much as for retail users. Treasury movement, supplier payments, and cross border settlement are all practical growth paths.

Credit and real estate remain large long term opportunities. Their path will be slower. These categories need tighter legal design, stronger servicing, and deeper liquidity to scale. That does not weaken their importance. It means product quality will matter more than narrative. The winners in these sectors will likely be platforms that make legal rights, reporting, and redemption terms very clear from day one.

Rights based assets may shape the longer edge of the market. IP, research rights, and creator economics speak to a broader change in ownership models. These products are still early, yet they point to a future where tokenization plays a role in funding and managing assets that do not fit neatly into old financial wrappers. That part of the market will need strong legal discipline and patient capital. It still deserves close attention.

The broader direction is clear. The market is shifting from isolated tokenized products toward connected systems. Infrastructure, assets, payments, reporting, and applications are starting to link more tightly. That does not mean every asset will move onchain. It does mean the assets that gain real value from faster settlement, better records, wider distribution, or programmable use will keep moving in that direction.

Conclusion

The RWA market is best understood as a connected system. Infrastructure lays the rails. Asset issuers bring value onchain. Applications turn that value into usable products for investors, firms, and consumers. This view is much more useful than a narrow focus on one product class.

Tokenized Treasuries lead the market today, and they deserve that role. They offer a clear asset, a known yield profile, and a strong fit for digital treasury activity. Yet the wider market reaches far past Treasuries. It now includes commodities, credit, real estate, payment tools, collectibles, fan assets, rights based products, and machine resource markets. Each category serves a different need. Together, they show what tokenization can do in practice.

The strongest lesson is simple. A good RWA product is not just a token on a chain. It is a legal claim, a data system, a transfer model, and a user product working in one structure. That is why infrastructure matters so much. That is why legal clarity matters so much. And that is why the next phase of growth will favor products that solve real market problems in a clear and durable way.

real estate asset tokenization is gaining attention in 2026 because it speaks to practical market problems such as limited access, high entry barriers, slow transactions, and fragmented investment processes. Startups are building platforms around it not just to offer digital property fractions, but to support issuance, compliance, investor management, and secondary market activity within a more organized framework. As interest in real-world asset digitization continues to grow, businesses that want to enter this space will need the right technical and strategic support to move from concept to execution. Blockchain App Factory provides RWA Tokenization Services for businesses looking to develop secure and market-ready solutions in this growing segment.